Manage account

Professional management of investment accounts. Use all our know-how to manage your investment account.

Expected fund indicators

Jak to funguje zpráva investic

We are a quantitative investment management company trading equities around the globe.

- Quantitative:Using advanced statistical and machine learning models.

- Systematic:100% following models.

- Efficient:Cost-effective execution of strategic trades.

Proč je dobré svěřit nám správu inveestičních účtů

We invest into publicly traded stocks from developed markets, including U.S., Canada, Europe, Japan, Australia, etc.

Investment universe as broad as ours offers a greater number of mispriced investing opportunities as well as stronger diversification relative to other regionally restricted strategies.

Our exposures to individual countries and regions varies over time and is fully dictated by the model.

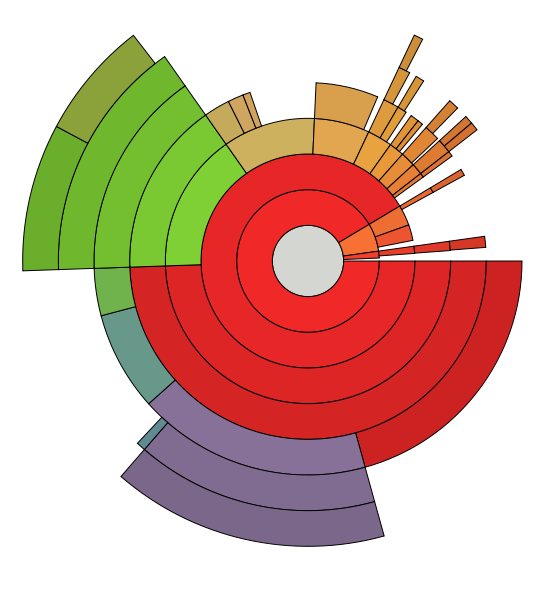

Regional and country decomposition of our portfolio for 31.12.2019 can be seen on the left.

TODO: add real multi-level pie-chart (regions and countries)

Poplatky za správu investičního účtu

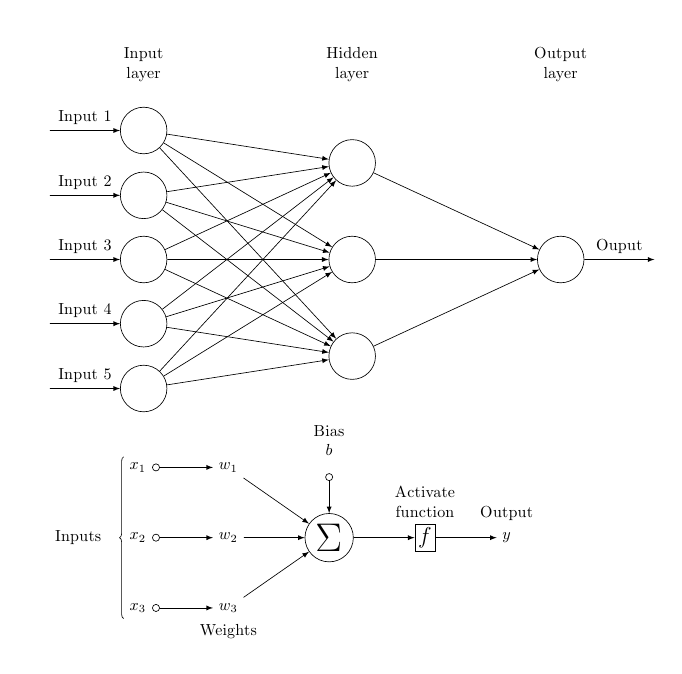

We use ensembles of state-of-the-art machine learning models:

- Neural Networks

- Gradient Boosted Regression Trees

- Random Forests

... in multiple prediction tasks:

- Excess stock returns

- Rank of the stock returns

- Classification of extreme stock returns

... tested in the rigorous statistical setting.

Pro koho je zpráva investic vhodná

Expectations based on the evidence from the large-scale data on equities from around the globe going back to 1926.

More than 50 000 firms from:

- North America (U.S., Canada)

- Europe (Austria, Belgium, Denmark, Finland, France, Germany,Greece, Ireland, Italy, Luxembourg, the Netherlands, Norway,Portugal, Spain, Sweden, Switzerland, and the United Kingdom)

- Japan

- Asia Pacific (Australia, New Zealand, India, and China)

Academic papers we read

We continuously monitor academic research and closely cooperate with researchers from universities.

Peek into our library:

- Lewellen, Jonathan, Stefan Nagel, and Jay Shanken. "A skeptical appraisal of asset pricing tests." Journal of Financial economics 96, no. 2 (2010): 175-194.

- DeMiguel, Victor, Lorenzo Garlappi, and Raman Uppal. "Optimal versus naive diversification: How inefficient is the 1/N portfolio strategy?." The review of Financial studies 22, no. 5 (2007): 1915-1953.

- Srivastava, Nitish, Geoffrey Hinton, Alex Krizhevsky, Ilya Sutskever, and Ruslan Salakhutdinov. "Dropout: a simple way to prevent neural networks from overfitting." The journal of machine learning research 15, no. 1 (2014): 1929-1958.

Technology stack

“One can predict the course of a comet more easily than one can predict the course of Citigroup’s stock. The attractiveness, of course, is that you can make more money successfully predicting a stock than you can a comet.”

Jim Simons, Renaissance Technologies